|

If central banks wait until their bonds mature on their balance sheet, they no longer have "unlimited capital" at their disposal and run the risk of the markets challenging the central banks.

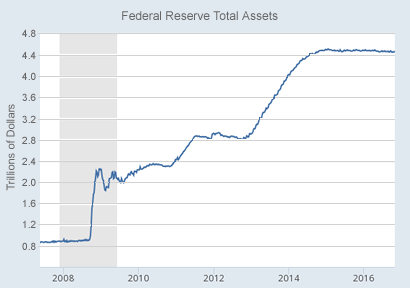

Once Quantitative Easing (QE) is done, the central banks can begin to normalize the money supply by reducing its balance sheet through Quantitative Tightening (QT).

During QE the central banks provide capital to support the banking system during times of illiquidity.

These additional cash balances creates an over supply of bank reserves and the

Natural Equilibrium of Interest Rates drives short term interest rates to 0%.

This has the additional effect of weakening the currency as the central bank essentially prints money to pay for the QE.

When the central bank begins quantitative tightening short term rates are naturally at 0% and the sale of bonds widens the yield curve which further supports the banking system.

The wider the yield curve gets the greater the profits are for the banks as they borrow short term to lend long term.

Not until excess bank reserves are at a supply and demand equilbrium of 0 will we see short term rates rise as the natural equilibrium drives interest rates higher as demand increases

pricing in the implied inflation rate.

Recently, central banks have push the boundaries of QE by driving debt to historically low levels to support unsustainable sovereign debt and force their economies to reignite with cheap capital.

Given the non linear and parabolic Impact of Monetary Policy at 0%, negative interest rates are deflationary and should be avoided.

|